The current downward pressure on the economy is relatively large, and the glass industry is facing serious overcapacity problems. Coupled with the arduous task of environmental protection, the glass industry urgently needs to be transformed and upgraded to solve the development dilemma. On the other hand, the return of manufacturing industry around the world, the proposal of the Industry 4.0 strategy, the introduction of the national “Belt and Road” strategy and the arrival of the new economic normal have created an unprecedented concept for the transformation of the glass industry. opportunity. The following is the development opportunity of the glass industry in 2017 summarized in the report hall " 2016-2021 China Glass Industry Special Investigation and Investment Value Forecast Report" .

Policy strategy drives the development of the glass industry:

1. The return of global manufacturing and the proposal of Industry 4.0 strategy

Since the outbreak of the international financial crisis, developed countries such as Europe and the United States have re-recognized the impact of manufacturing development on economic growth. After Obama screamed the slogan of “returning to manufacturing”, developed countries have put “re-industrialization” on the agenda. The US government has proposed to revitalize the manufacturing strategy, and has introduced a number of supportive policies for manufacturing, and the trend of manufacturing reversal has accelerated. Germany has proposed the "Industry 4.0 " strategy, and is planning to develop relevant laws to promote Industry 4.0 , and to upgrade Industry 4.0 from an industrial policy to national law. Once the day did not fall to the empire - the United Kingdom, its government technology office also strongly launched the "British Industry 2050 Strategy." French President Hollande set up the Ministry of Production and Revitalization, which aims to revitalize French industry and promote French re-industrialization. The Japanese government is adjusting its industrial layout with the intention of using artificial intelligence technology as an entry point to promote the revival of Japanese manufacturing.

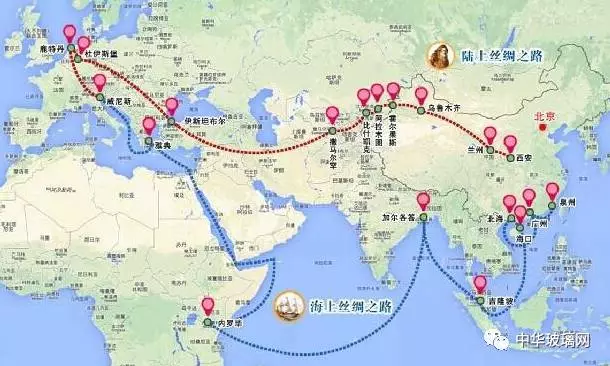

2 , "One Belt, One Road" strategy

2013 Nian 9 months, Xi Jinping proposed to jointly build the "Silk Road Economic Belt" speech at Nazarbayev University in Kazakhstan; the same year, 10 months, Xi Jinping expressed willingness ASEAN countries to enhance maritime speech at Indonesia's parliament Cooperation to jointly build the "Maritime Silk Road" in the 21st century. The “Belt and Road” strategy is China’s first historic regional economic integration strategy that actively affects the international order. It will promote the transformation of the domestic regional economy along the transportation corridor to the economic development zone, and use its good location advantages to promote regional economics along the route. The rapid development has fully utilized its growth and demonstration functions.

From the demand side, the countries along the “Belt and Road” countries, whether from domestic demand or future regional economic cooperation, are extremely demanding for infrastructure construction. Countries in Asia and Africa have 10 % and 20 % urbanization improvement space respectively compared with China , and China's accumulated experience and product and service capacity in the process of urbanization can be exported. From the domestic point of view, the density of railways, highways and highways in all provinces and regions in the northwest is ranked behind in the country. In order to realize the infrastructure docking between the “Belt and Road” countries, the infrastructure construction in the northwest of China, such as urban construction and transportation network, is very There is space.

From the perspective of the supply side, with the growth rate of fixed asset investment, the problem of overcapacity in China's construction industry and manufacturing industry is becoming more and more serious. The “infrastructure output” can greatly alleviate the pressure on product demand in China's construction industry and manufacturing industry. Under the background of the “One Belt, One Road” strategy, China’s participation in the establishment of the “BRICS Development Bank” and the “Asian Infrastructure Investment Bank” largely demonstrates the strategic concept of China’s expansion of its infrastructure investment business. The use of construction enterprise output methods can drive the output of domestic design, consulting, manufacturing, materials, labor, finance, insurance, services and other industries, and hedge domestic demand decline.

3 , "Made in China 2025 " strategy

China has the advantage of expanding Industry 4.0 . It is the only country in the world that has all the industrial categories in the UN industry classification. It has formed an industrial system with complete and independent categories. This large and complete industrial system relies on the agglomeration effect of many industrial enterprises. It is highly flexible and paves the way for the realization of “Industry 4.0 ” in the future . At the same time, China is not only an important producer of products, but also one of the world's largest consumer markets. This dual role will enable the domestic market to have stronger interaction with industrial production, promote social and economic development, and help defend the world. The impact of economic fluctuations.

"Made in China 2025 " is the Chinese version of "Industry 4.0 " plan, plan by Prime Minister Li Keqiang issuing, by the State Council in 2015 Nian 5 Yue 8 publication date. "Made in China 2025 " will design a top-level plan and roadmap for China's manufacturing industry in the next 10 years, and strive to achieve the transformation of China's manufacturing to China, China's speed to China's quality, and China's products to Chinese brands.

New economic normal new opportunities

The above is the policy strategy to promote the development of the glass industry, then what are the development opportunities for the glass industry in the market itself? According to the report analysis, under the new economic normal, the development opportunities of the glass industry can be classified into two major aspects: demand and supply:

First of all, the demand side.

The main demand for the glass industry is construction, automotive, home electronics, and so on.

1 , construction needs. As a country with a large population, China's housing demand is also a huge data. The huge population is accompanied by eating, drinking and living. This is also an opportunity for the glass industry from the side.

According to the report , China's residential area reached 40 billion square meters in 2010 , and this data is also constantly rising. China's urban area has increased by an average of 11 per year . 2.5 billion square meters. The demolition and renovation of old houses and the construction of new houses are also indispensable for the demand for glass. In particular, urban buildings are mainly based on glass buildings to win people's love.

If you need 0 per square meter of construction . 4 square meters of glass calculations. Only a year had demand for glass 4 . 5 Yi square meters (about 9 , 000 million boxes).

The rise of second- and third-tier cities has increased the demand for glass. According to national census data show that the population has a 6 , 000 provincial units Wan about point of view, the new urban area per year 3 , 542 square meters. In 2011 , many provincial capital cities and developed cities in China have begun to gradually use energy-saving and environmentally-friendly insulating glass. There are also more demands in the category of glass.

2 , automotive industry demand. From the perspective of China's auto industry, the rapid rise of China's auto industry has brought good news to the glass industry. The Chinese auto industry such as BYD, Chery, Great Wall and Jianghuai started late, but the production capacity is relatively large. 2013 annual output has exceeded 2 , 000 million. As the performance of automobiles improves, the proportion of glass in automobiles has also increased significantly. In 1990 , the demand for glass per car was 3 per vehicle . About 5 square meters; in 2000 , the demand for glass per car was 3 . About 85 square meters; currently, at least 4 square meters of glass per car .

Glass can make the car look more beautiful, reduce the resistance during driving, and greatly reduce fuel consumption. The performance of the glass at each position on the car is also greatly different, and the technical requirements for the material of the glass are different. According to different uses, it can be divided into: safety glass, laminated glass, tempered glass, and regional tempered glass. It takes a lot of cost to take and process a single glass.

In the glass consumption of auto parts, on the one hand, the glass is recycled; on the other hand, the Chinese glass market is not fully adapted to the balance between supply and demand. This is a stimulus for the glass industry.

3. Demand for electronic products. Electronic products in daily life, such as mobile phones, computers, televisions and other highly informational high-tech products, rely more on ultra-thin sensitive glass. They are extremely demanding on glass, free of impurities, abrasion, sun, cracks, and so on. Only 2000 years ago, our country in order to develop electronic products, the introduction of ultra-thin glass have 1 , 000 square meters. Then the demand for glass for home electronics is increasing year by year. 2015 annual demand for ultra-thin glass had 2 , 000 square meters. If we add up the demand for glass involved in our lives, this number will be even larger.

Second, the supply side.

1. Architectural glass has certain requirements in terms of wind resistance, snow resistance, and impact resistance. For the control of light transmittance and satin stripes, it is not as strict as that of automobiles and electronic products.

China's architectural glass technology is in the forefront of the world in terms of wind resistance and snow resistance. Therefore, China is mainly self-supply for architectural glass. However, China's economy is developing rapidly and its quantity is large. It still needs to rely on imports to meet the huge market demand.

2 , for automotive glass, electronic products, ultra-thin glass, etc.requires a high level of technology. China's Fuyao Glass, Yaohua Glass, Jinjing Glass and other leading companies are relatively mature in the control of automotive glass technology, but the core technology property rights are not in China, and automotive bulletproof glass and insulating glass still need to be imported in large quantities. There are serious supply shortages in ultra-thin glass, radiation-proof glass, and anti-UV glass for electronic products. With China's economic growth, demand will become larger and larger, and it is unrealistic in the long run to rely on imports to meet domestic demand.

All in all, in 2017 , the glass industry has great opportunities for development both in policy and in economics. The key is whether glass companies can seize this opportunity and quickly realize transformation and upgrading to meet market demand.

Guangdong Provincial Association of Industry Associations 20… Hand in hand, create brilliant, 2018 Starlight annual meetin… Home decoration uses art glass to create a personal space Celebrating the 38th Goddess Festival Tour of Douyama Town, Doosan Town, Taishan City Taifeng City Duanfen Meijia Courtyard Tour Starlight Glass has become the governing unit of Guangdong B… Analysis of the transportation environment of float glass ma…

Guangdong Provincial Association of Industry Associations 20… Hand in hand, create brilliant, 2018 Starlight annual meetin… Home decoration uses art glass to create a personal space Celebrating the 38th Goddess Festival Tour of Douyama Town, Doosan Town, Taishan City Taifeng City Duanfen Meijia Courtyard Tour Starlight Glass has become the governing unit of Guangdong B… Analysis of the transportation environment of float glass ma…

Previous:

Previous: